Structured Notes in a Separately Managed Account: Converting Market Volatility Into High Monthly Income

- Apr 29

- 5 min read

Updated: May 4

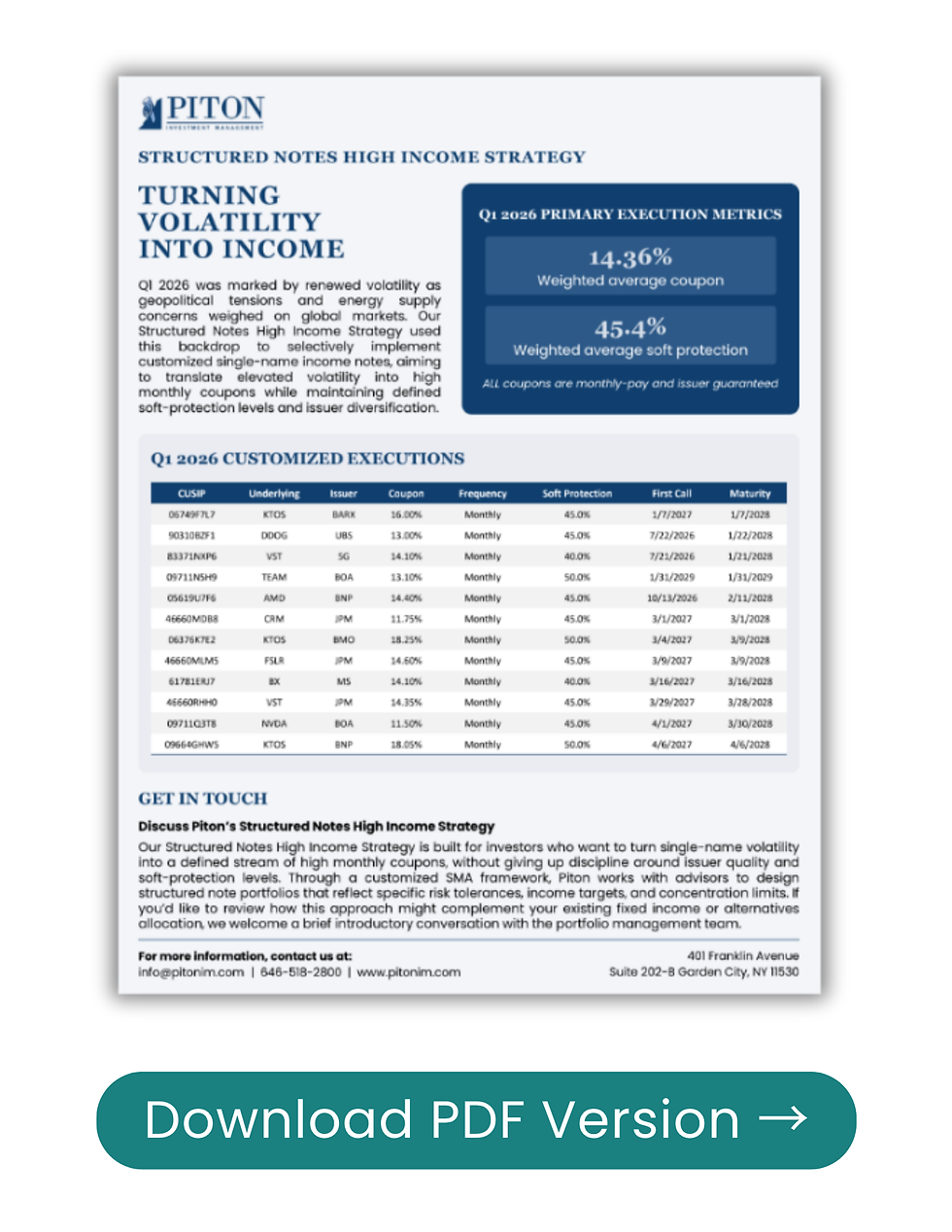

Equity volatility, which most investors treat as a liability, generated a 14.36% weighted average coupon for structured note portfolios in Q1 2026. That gap between conventional fixed income yields and what a disciplined structured notes strategy can produce is no longer marginal. For RIAs, wealth advisors, family offices, and institutional allocators searching for customized fixed income solutions, it is worth understanding precisely how the conversion works.

How Volatility Becomes an Income Mechanism

Single-name equity volatility remained structurally elevated through much of early 2026, driven by geopolitical pressures, sector rotation, and energy supply uncertainty. For fixed income allocators looking to complement an existing portfolio with a differentiated income source, that environment created a meaningful opportunity. Structured notes convert implied volatility into a defined coupon.

The higher the implied volatility on a given underlying, the higher the coupon a note issuer is willing to guarantee, provided the structured note's terms clearly define the investor's risk exposure through a soft protection buffer. Volatility that might otherwise sit as background noise in a broader portfolio becomes, within this structure, the direct driver of monthly income.

How Customized Structured Notes Generate Yield

A customized structured note is a debt obligation issued by a financial institution, tied to the performance of a single underlying equity. The investor receives a fixed, guaranteed monthly coupon. In exchange, they accept contingent downside exposure below a defined soft protection threshold, typically 40% to 50% below the underlying's initial price.

The mechanics are straightforward. If the underlying closes above the soft protection barrier at maturity, the investor receives full principal and all coupons. If the underlying breaches the barrier, the investor participates in that decline. The coupon compensates for accepting that contingent risk over the note's term.

Within a separately managed account structure, these notes can be customized across five key dimensions: underlying selection, issuer, coupon rate, protection level, and maturity date. That flexibility is the defining advantage of structured notes in an SMA versus purchasing off-the-shelf notes in the secondary market.

Q1 2026 Execution: Real Structures, Real Numbers

To make this concrete, consider the range of structures executed during Q1 2026. Coupons spanned from 11.50% on an NVDA-linked note issued by Bank of America, carrying 45% soft protection, to 18.25% on a KTOS-linked note issued by BMO, with 50% soft protection. Every note in the portfolio paid monthly and carried an issuer guarantee from a major financial institution, including JPMorgan, UBS, Societe Generale, BNP Paribas, Morgan Stanley, and others.

The diversity of issuers matters. Concentrating structured note exposure in a single bank introduces counterparty risk, undermining the discipline of the overall fixed income SMA. A properly constructed portfolio distributes that exposure across multiple highly rated institutions.

Portfolio Construction Principles for a Fixed Income SMA

Yield-enhanced fixed income through structured notes is not simply about chasing the highest coupon available. A disciplined approach to portfolio construction considers four factors simultaneously.

Underlying selection

The most productive structured notes tend to come from underlyings with elevated single-name implied volatility and clear institutional coverage. Names without sufficient options market liquidity may offer attractive headline coupons but carry execution risk that erodes realized returns.

Protection calibration

Soft protection levels should reflect the investor's actual risk tolerance and the underlying's historical drawdown behavior. A 40% barrier on a name with a history of 50% peak-to-trough declines is a different risk proposition than the same barrier on a more stable underlying.

Issuer diversification

No single counterparty should represent an outsized share of portfolio notional. The SMA structure allows advisors to set explicit issuer concentration limits as part of the investment policy, something unavailable when purchasing notes through brokerage platforms.

Maturity laddering

Staggering first call dates and final maturities across the portfolio creates a predictable reinvestment schedule and reduces the risk that a large portion of the portfolio calls simultaneously into a lower-volatility environment.

Why the SMA Structure Matters for Sophisticated Investors

The separately managed account format is not a detail. It is the feature that makes customized structured notes appropriate for RIAs and family offices who have fiduciary responsibilities and client-specific parameters to honor. Every note in the SMA is titled in the client's name. The advisor retains full transparency into position-level detail. And the portfolio can be constructed to reflect specific income targets, concentration limits, and maturity preferences that a pooled vehicle cannot accommodate.

For investors who have historically allocated to alternatives or private credit for yield, the fixed income SMA with structured notes offers comparable return potential with daily liquidity at the position level and a clearly defined risk structure. That combination is difficult to replicate elsewhere.

Integrating Structured Notes Into an Existing Allocation

The most natural entry points for a structured notes SMA are as a complement to existing fixed income or as a partial replacement for alternatives exposure. The monthly income characteristic aligns well with distribution requirements. The defined risk structure, anchored by the soft protection barrier, makes structured notes more transparent than many credit hedge fund strategies that carry comparable return targets.

For advisors evaluating yield enhanced fixed income for client portfolios, the primary due diligence questions center on underlying selection discipline, issuer quality standards, and the manager's ability to source competitive terms across market environments, including lower-volatility periods when coupon levels compress.

See our Comprehensive Guide on Structured Notes

Piton's Structured Notes primer provides a detailed framework for evaluating structured notes within a fixed income allocation. To discuss how a customized structured notes SMA might complement your clients' fixed income allocation, contact us at info@pitonim.com.

Disclosure

The Piton Structured High Income average portfolio coupon represents current gross yield to worst for all current structured notes currently issued. The coupon numbers shown do not reflect potential deductions of investment advisory fees, brokerage or other commissions, and any other expenses that a client may have paid. The fees and expenses charged in connection with these structured notes may be higher than the fees and expenses of other investment alternatives and will reduce profits and increase losses. It should not be assumed that any structured notes will prove to be profitable. The current portfolio information provided herein is current as of the date of this composite. Structured notes are complex products and are not suitable for all investors. Before making any investment decision, you should carefully consider the investment objectives, risks, charges, and expenses before investing. This and other important information are included in the structured notes’ offering documents. The structured notes discussed herein are presented strictly for informational purposes and should not be construed as a recommendation to buy or sell. For further information regarding Piton Investment Management, LP, please see our Form ADV at www.sec.gov.